For many individuals whose houses are battered by a hurricane or tropical storm, the trauma is quickly adopted by one other main supply of stress: coping with their insurance coverage firm to file a declare.

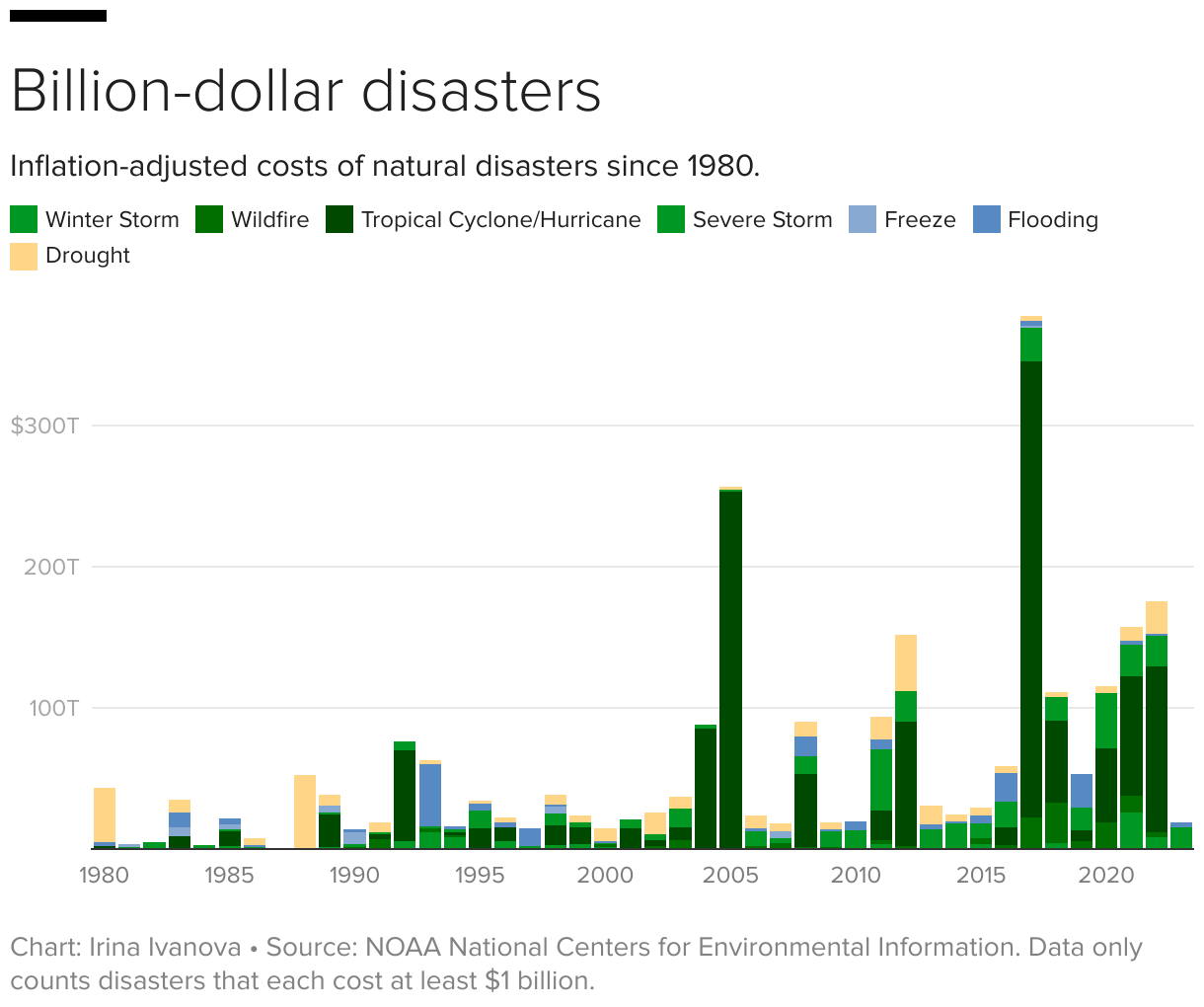

The U.S. suffered 20 separate billion-dollar climate and local weather disasters in 2021, with a complete price of $145 billion, in keeping with the Nationwide Oceanic and Atmospheric Administration. Particular person owners whose properties are hit by a hurricane can undergo tens of hundreds of {dollars} in harm, or much more, relying on the severity of the storm.

And the remnants of Tropical Storm Hilary delivered record-breaking rainfall to Southern California this week, flooding roads and inflicting mudslides, and will additionally trigger flooding in Oregon and Idaho.

Understanding the fundamentals about owners insurance coverage and submitting a declare can assist keep away from some pitfalls if catastrophe strikes. As an illustration, such insurance coverage will sometimes cowl harm from robust winds, however some insurance policies do not cowl windstorms. Usually, property homeowners can have a separate deductible for hurricanes, so it pays to test what your coverage covers — and, equally necessary, what it would not — earlier than a storm hits, specialists say.

“It is good to look it over if you renew,” Vince Perri, founder and CEO of Elite Resolutions and a public insurance coverage adjuster, informed CBS MoneyWatch.

This is what to learn about hurricane insurance coverage and the best way to take care of your insurer after a catastrophe.

Examine your hurricane deductible

Hurricane deductibles sometimes quantity to between 2% and 10% of the overall worth of your house. However in hurricane-prone areas like Florida, the place Perri is predicated, he recommends getting a decrease deductible due to the chance of dealing with excessive out-of-pocket prices in a catastrophe.

“Somebody despatched me a coverage to assessment and he was going to go along with 10% — I informed him, ‘Do not try this, as a result of sadly we get hurricanes on a regular basis’,” he stated.

As an illustration, a house price $400,000 with a ten% deductible might face out-of-pocket prices of $40,000 if the property had been worn out. Going with a decrease deductible might cut back incremental prices, however result in monetary catastrophe in case of great harm.

“You need a 2% deductible with regards to hurricanes,” Perri suggested.

Doc your house earlier than the storm

Every year, owners ought to stroll round their property and take images to doc their dwelling’s situation, Perri really useful. Taking this step will allow you to after a storm as a result of you can exhibit to your insurer that the harm was truly brought on by the hurricane.

“If there’s a storm, the insurance coverage firm might need to say the harm they’re seeing will not be because of the hurricane however is pre-existing,” he famous. “In case you have proof, that might allow you to tremendously.”

Take images instantly after a hurricane

After a storm, take images of the harm as rapidly as attainable to doc the rapid aftermath of the hurricane. Below a provision in owners insurance coverage referred to as “Duties After Loss,” that is sometimes a part of a house owner’s accountability after a catastrophe.

Different steps you may have to take beneath this clause might embrace submitting a declare promptly, defending the property from additional harm and authorizing the insurance coverage firm to examine your property. Examine your coverage to ensure you perceive your duties in case of a storm.

File your declare rapidly — and comply with up

Some insurance coverage insurance policies require you to file your declare in a well timed method, however most householders are doubtless going to need to file as quickly as attainable as a way to expedite fee. To that finish, be sure to comply with up along with your insurance coverage firm at the least each seven days after submitting a declare, Perri recommends.

After a hurricane or different catastrophe, “They have lots of of hundreds of insurance coverage claims, so when you do not comply with up, you would get forgotten,” he added. “The squeaky wheel will get the grease.”

You do not have to simply accept your insurance coverage firm’s first provide

An insurer will both deny a declare, or settle for it and make a fee — nevertheless it may not be an quantity that you just consider is sufficient to restore the harm to your house. In that case, you possibly can file an enchantment.

To try this, you possibly can ask for estimates from contractors and submit these as proof the proposed fee is just too low, or rent a public insurance coverage adjuster who works for you, the house owner, slightly than the insurance coverage firm. Public insurance coverage adjusters usually cost a charge of between 5% and 20% of the insurance coverage declare.

“Rent any individual that places these estimates collectively that you should utilize to enchantment,” Perri stated.

In case you use a contractor, be sure the estimate is extraordinarily detailed, right down to the variety of coats of paint they may use to revive your home to its former state, he suggested. “Documentation is king,” Perri added.